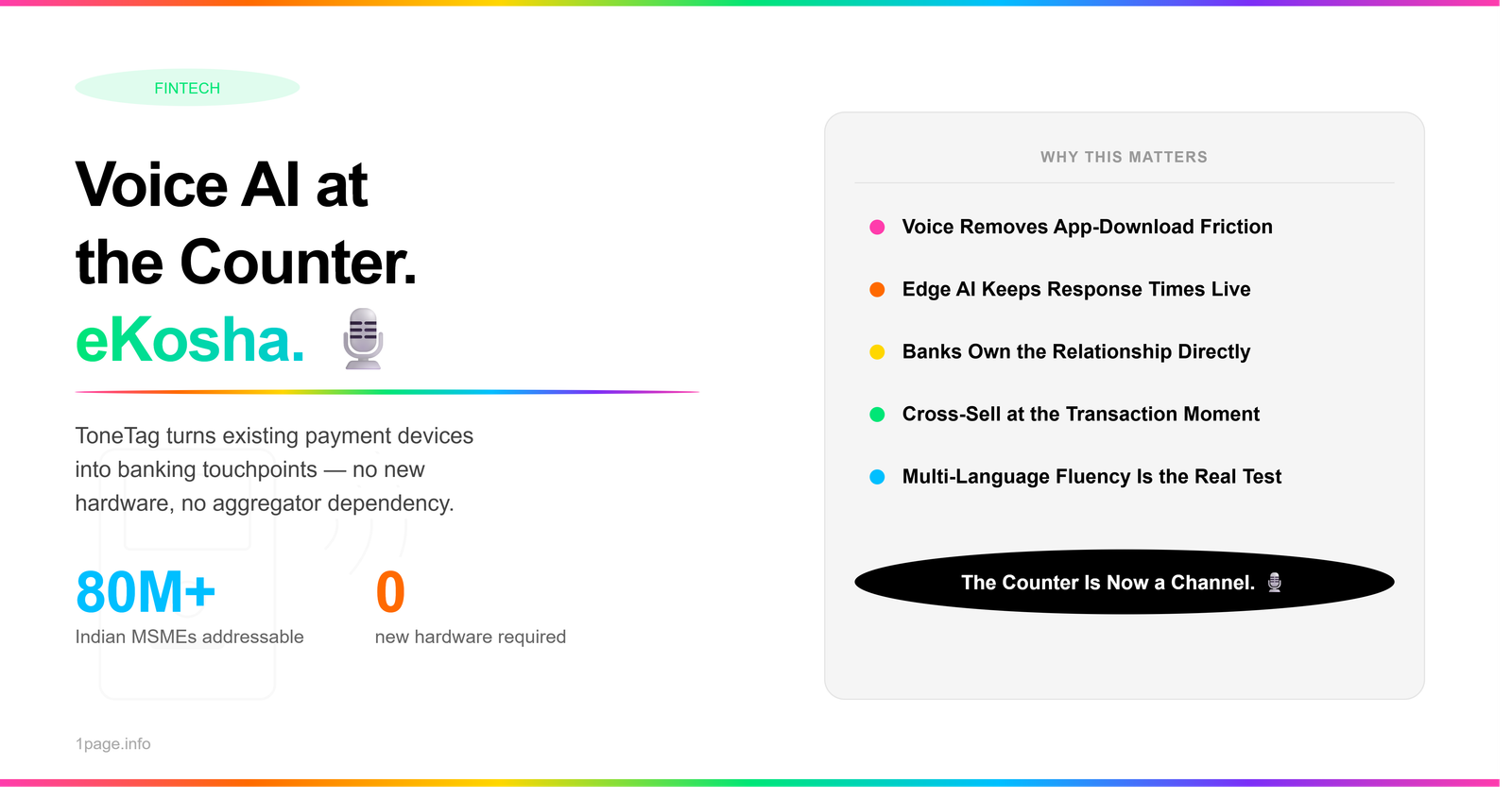

Every payment counter in India could soon double as a banking branch. That's the bet behind eKosha, the voice-first AI business assistant ToneTag launched this month. Built on the company's Edge AI technology, eKosha turns existing payment acceptance devices into banking touchpoints without new hardware. Banks get a way to reach over 80 million MSMEs through a device merchants already use daily. No new terminals. No separate app download. Just voice, at the counter, during a transaction merchants are already completing.

This matters for anyone marketing fintech or banking products right now. The distribution problem that's plagued merchant banking for a decade — reaching small businesses without expensive field sales — just got a plausible answer.

What Does eKosha Actually Do at the Payment Counter?

eKosha sits on top of payment acceptance devices banks already have in the field. A merchant swipes a card or scans a QR code. The same device, powered by Edge AI, can now hold a voice conversation about a working capital loan, a savings product, or a cross-sell offer relevant to that merchant's transaction volume.

This is different from a chatbot bolted onto a banking app. Most merchants running a shop counter don't have time to open an app, navigate menus, and read through product terms. Voice removes that friction. The merchant talks. The device responds. The transaction that was already happening becomes the moment a bank pitches a product.

Edge AI processing matters here too. Running the intelligence locally on the device, rather than routing everything through a cloud call, keeps response times fast enough for a live counter interaction. A three-second lag kills a voice interface. Banks testing merchant tools have learned this the hard way.

Why Are Banks Chasing MSME Distribution This Hard?

India has more than 80 million MSMEs. Most of them are underbanked in ways that go beyond just lacking a loan. They lack ongoing engagement. A merchant might have a business account they opened once and never touch again beyond basic transactions.

Third-party aggregators have filled this gap for years — and taken a cut for doing it. Every merchant banking relationship routed through an aggregator is a relationship the bank doesn't fully own. Data stays with the aggregator. Cross-sell opportunities stay with the aggregator. The bank becomes a backend processor.

eKosha's pitch to banks is straightforward: own the merchant relationship directly, at the point where the merchant is already present and transacting. Reduce dependence on the middlemen who've been collecting the margin on merchant engagement.

Have you noticed how many fintech products claim to solve distribution but really just add another app to a merchant's phone? That's the trap. eKosha's design choice — building on infrastructure that already exists at the counter — avoids adding friction rather than removing it.

What Does This Mean for Fintech and Banking Marketers?

If you're marketing merchant banking products, the counter just became a media channel. Product messaging that used to live in app notifications or SMS campaigns can now happen conversationally, in the moment a merchant is thinking about cash flow.

This changes what conversion looks like. A merchant hearing about a working capital line while completing a sale is a warmer moment than a push notification they'll dismiss later. Financial products pitched at the point of transaction convert differently than products pitched through cold outreach. The merchant is already thinking about money movement. The offer arrives at a relevant instant instead of an interruption.

Banks adopting tools like this will need marketing that's less about driving app downloads and more about training merchants to expect and trust voice interactions at their existing devices. That's a different skill set than most banking marketing teams have built so far.

Region and language matter enormously here too. A voice assistant that only works well in English misses most of the addressable market. eKosha's value depends heavily on how well it performs across the languages merchants actually speak at their counters — Hindi, Tamil, Bengali, Marathi, and dozens more. Marketing this product convincingly means demonstrating that fluency, not just claiming it.

CLOSING: eKosha turns a transactional moment into a relationship-building one, giving banks a direct line to India's MSME base without new hardware or aggregator dependency. For marketers, this shifts merchant banking promotion from app-download campaigns toward point-of-transaction trust-building — worth understanding before competitors figure it out first. Read more fintech breakdowns like this at 1page.info