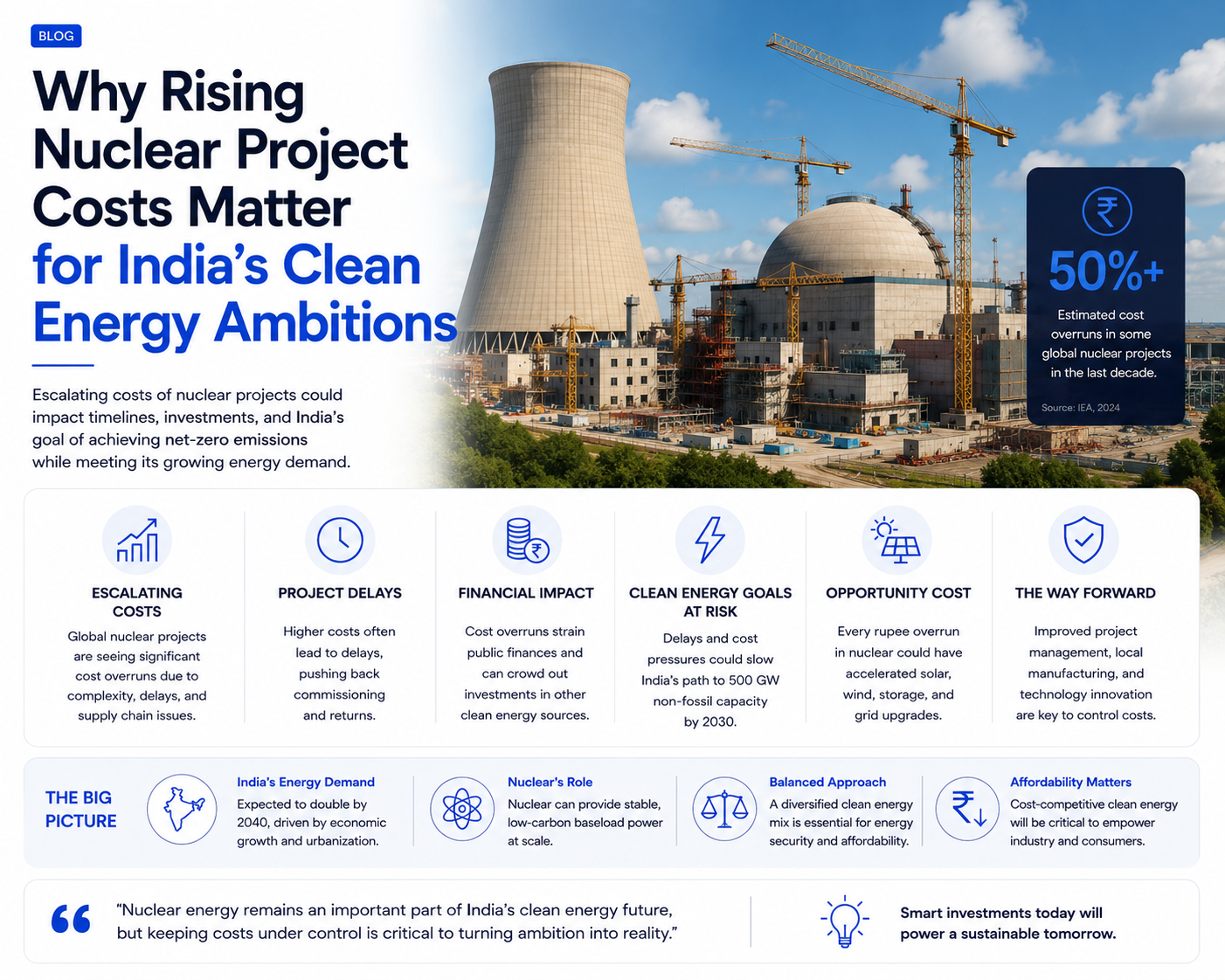

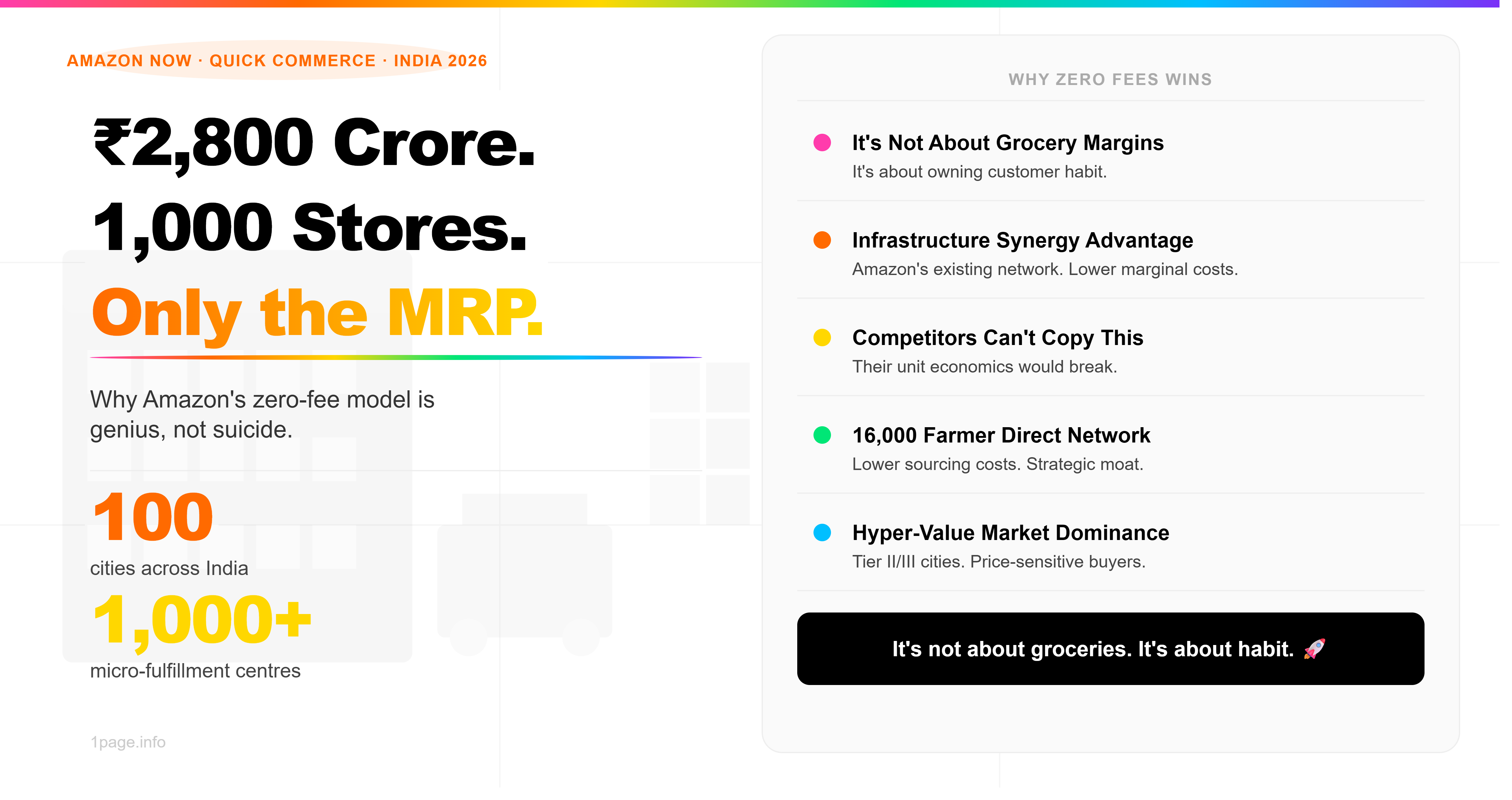

Amazon just committed ₹2,800 crore to expand Amazon Now across 100 cities in India, backed by 1,000 micro-fulfillment centres. The move seems reckless on paper. Grocery margins are already razor-thin. Delivery infrastructure costs are massive. And Amazon is charging customers exactly what the product costs — nothing more.

When Blinkit, Zepto, and Swiggy Instamart are charging convenience fees, delivery fees, and platform markups on every order, Amazon's zero-fee model looks like a company trying to lose money.

It's not. It's the smartest play in quick commerce right now.

The Real Prize Isn't Grocery Sales — It's Customer Habit

The quick commerce market in India crossed ₹11,000 crore in January 2026, growing 100% year-over-year. That sounds massive until you realise something important — 95% of quick commerce orders are still groceries and daily essentials. The margins are terrible. The unit economics barely work.

But that's not what Amazon is actually chasing.

What Amazon is building is customer habit. When you can open the Amazon Now app and get anything you want in 10 minutes for the exact MRP — no hidden charges, no fees — you start opening that app for everything. Not just groceries. Not just in emergencies. As your default.

That's the lock-in. That's where the real value is.

Blinkit operates with a convenience fee. Zepto charges delivery. Swiggy Instamart has platform markups. Every order, customers are paying 15-30% more than the MRP. With Amazon, they're not. The psychology matters enormously. Over time, that psychological advantage compounds.

The Unit Economics Play — Why Absorbing Losses Now Makes Sense

The quick commerce sector has a fundamental problem — unit economics barely work at scale. Delivery costs, warehouse operations, inventory holding — all of it eats into margins that don't exist.

But here's what Amazon understands that competitors don't: this is not a quick commerce business. It's an infrastructure play disguised as a quick commerce business.

Amazon already operates massive fulfilment centres, last-mile delivery networks, and logistics infrastructure across India. When Amazon Now delivers a product, it's using infrastructure that Amazon has already built and paid for (or is amortizing across multiple business lines — retail, AWS, third-party logistics). The marginal cost of a quick commerce delivery is far lower for Amazon than it is for Blinkit or Zepto, which are pure-play quick commerce companies.

By charging zero fees, Amazon is operating closer to break-even on quick commerce alone — while Blinkit and Zepto are losing significant money per order. Over a 3-5 year period, Amazon can absorb these losses while competitors burn cash and slow down.

Then — once market consolidation happens and unit economics improve — Amazon can expand margins. By then, habit is locked in, and customers have no reason to switch.

The 16,000 Farmer Direct Connection — The Strategic Moat

Here's a detail most people missed: Amazon Now connects over 16,000 farmers directly to customers. Blinkit and Zepto don't have this.

Direct farmer relationships mean direct sourcing. Direct sourcing means lower procurement costs. Lower costs mean Amazon can afford to offer zero fees while competitors need them to stay solvent. Over time, Amazon's supply chain becomes a competitive moat that money alone can't replicate.

Why Competitors Can't Copy This

Blinkit's model is to charge. Swiggy Instamart's model is to charge. Zepto's model is to charge. These business models are built on the assumption that convenience fees + delivery fees sustain the unit economics. They cannot drop those fees without fundamentally breaking their own economics. Their unit losses would become unsustainable.

Amazon can afford to do something competitors can't. That's the point.

The Broader Play — Hyper-Value Commerce

Amazon's zero-fee model plays directly into the hyper-value commerce trend dominating Indian e-retail. Hyper-value (items priced under ₹300-1000) has grown from 5% of India's e-retail market to 12% since 2021. And it's being driven primarily by Tier 2 and Tier 3 cities.

These are the exact cities Amazon Now is expanding to. And for price-sensitive customers in smaller cities, the MRP-only model is extraordinarily compelling. No hidden charges. No surprise fees. Just the price you see.

What This Means for Small Businesses, Retailers, and Grocers

For traditional retail and local grocers, this is a problem. Amazon's scale, unit economics, and zero-fee model will eat market share. Competition will be brutal.

But for businesses smart enough to adapt — partnering with Amazon Now as sellers, offering exclusive products, or building niche categories that Amazon doesn't dominate — there's opportunity.

The Bottom Line

Amazon isn't trying to make money on quick commerce. Not yet. It's trying to own customer habit, build a competitive moat through direct farmer relationships and logistics synergy, and position itself to dominate a market that doesn't yet exist at scale — where quick commerce isn't just groceries, but the first place Indians open an app for any small purchase.

By the time Blinkit, Zepto, and Swiggy realise what's happening, Amazon will have captured habits that are worth far more than the fees they're still charging.

That's why ₹2,800 crore looks like a bet worth making.